Most great businesses start as an idea, a passion project, a side-hustle tinkered with in the evenings and on weekends. It’s like building a custom car in your garage: you have the engine, the vision, and the drive. But going from side hustle to small business can feel like building a custom car. It requires a deliberate process of assembly, registration, and maintenance to transform your passion into a legitimate, road-worthy vehicle built for the long haul.

Many entrepreneurs believe that forming a business is the hard part. In reality, that’s just the beginning. Much like buying a car, the initial act is relatively straightforward; the real work lies in the ongoing maintenance, nurturing, and responsible ownership that follows. This guide is your owner’s manual for that journey. It will walk you through the four critical stages of building your business in Massachusetts, ensuring it’s set up for success from the beginning.

A quick note before we get started (my lawyer told me to add this… and that lawyer is me): This article provides general information for educational purposes only and does not constitute legal or tax advice. While the author is an attorney licensed to practice in Massachusetts, reading this article does not create an attorney-client relationship. Every business situation is unique, and you should consult with a qualified professional for advice tailored to your specific circumstances. This roadmap is provided to help you get started, but by all means is not all encompassing, and you will likely have additional considerations unique to your business.

We will cover:

- Choosing the Vehicle (Your Business Structure)

- Getting the VIN, Title, and Manual (Formalizing Your Business)

- Installing the Fuel and Safety Systems (Your Financial Infrastructure)

- Creating the Annual Maintenance Schedule (Ongoing Compliance)

- The DIY Route vs. Hiring a Professional: A Final Consideration

Part 1: Choosing the Right Vehicle: The Foundational Decision on Business Structure

The first and most critical decision in building your business is selecting the right legal structure. This choice is like deciding on which vehicle is right for your particular journey; it determines its fundamental characteristics, its cost, its complexity, and, most importantly, its level of safety i.e. your personal liability protection.

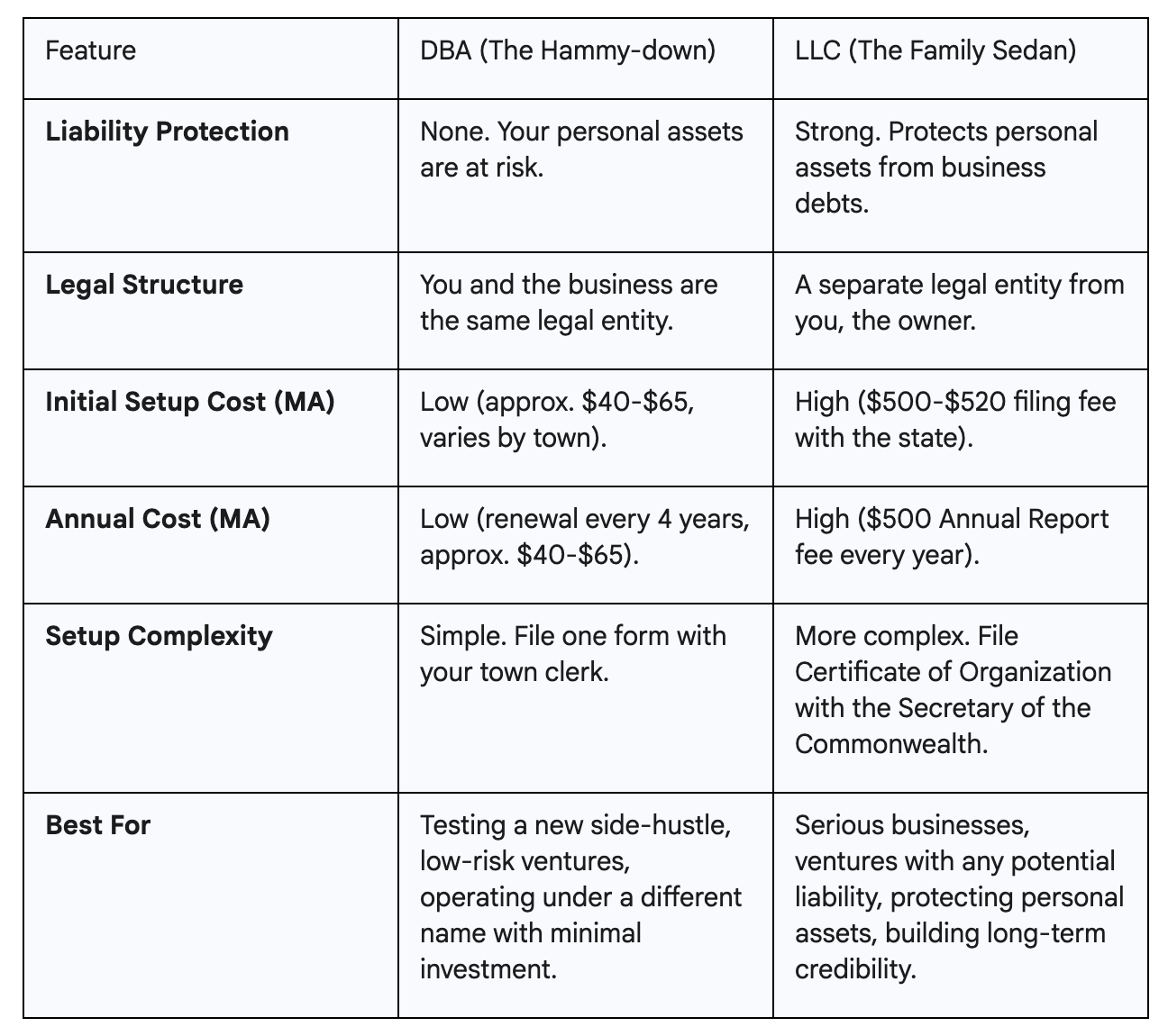

The hammy-down (Sole Proprietorship with a DBA)

When you first start earning money from a business activity, you are, by default, a sole proprietor. If you decide to operate under a creative or professional name, that is anything other than your own legal name, Massachusetts law requires you to file a Business Certificate, commonly known as a “Doing Business As” or DBA.

Think of the DBA as your first car. You know, the one that was passed down from siblings. It gets you from point A to point B. Is road legal, but perhaps lacks the advanced safety features of newer models. This vehicle is incredibly easy and inexpensive to get running, making it perfect for testing a business idea in your local market. The process is simple: you file a single form with your local city or town clerk, and the fee is typically low, ranging from about $40 to $65 depending on the municipality. If you are not operating under a trade name, then you can even forgo this step completely.

However, the hammy-down has its flaw: it offers absolutely no safety features. The DBA is only good for establishing a presence, evidence of your use of the business name, but even that is not the strongest evidence when we later think about registering the name with the State or for Trademark. Further, as a sole proprietor with a DBA, there is no legal separation between you and your business. You are the vehicle. If your business incurs debt or is sued, your personal assets, including your house, your savings, your real car are completely exposed and at risk. This is not meant to scare you, its just a reality you should know about when starting a business.

Buying a new car (The Limited Liability Company)*

The most common occurrence, one that provides you with some safety features is the Limited Liability Company (LLC). An LLC is a formal business structure that exists as a legally separate entity from its owner. This separation creates what’s known as the “corporate veil,” a powerful legal shield that protects your personal assets from business liabilities.

Think of the LLC as your reliable family sedan. It’s constructed with a strong steel chassis and equipped with updated airbags designed to protect the driver (you) and your passengers (your family and personal assets) in the event of a crash.

Building this safer vehicle in Massachusetts, however, comes with a price tag. The state requires an initial filing fee of $520 for the Certificate of Organization and a $520 annual report fee every single year thereafter. This financial hurdle forces entrepreneurs to be strategic. For many, the low-cost DBA becomes a necessary “beta-testing” phase to validate a business model before committing to the substantial investment an LLC requires. While a DBA is a great way to start, the LLC is the proper form for anyone committed to protecting their personal wealth while building a credible, sustainable enterprise.

*This roadmap does not cover other business entity types, of which there are a few.

Part 2: Getting Your VIN, Title, and Owner’s Manual: Formalizing Your Business Identity

Once you have selected the LLC, you must complete the official paperwork to make it a unique and legally recognized vehicle. This involves getting a federal Employer Identification Number (your VIN), state registration (your title), and an internal rulebook (your owner’s manual). These steps are not independent tasks; they must be completed in a specific sequence to properly formalize your business. Forgoing these critical, but often overlooked steps, is like buying your new car, and never changing the oil. A critical fault that renders the car, and in this metaphor the liability protection, useless.

The Title and Registration (State Filing)

The legal act that officially creates your LLC is the filing of a Certificate of Organization with the Massachusetts Secretary of the Commonwealth. This is the equivalent of going to the Registry of Motor Vehicles to get the official title and registration for your car. Until this document is filed and approved by the state, your business vehicle doesn’t legally exist and cannot be on the road. The $500+ filing fee is the state’s one-time “registration tax” to make your business official. It is a prerequisite for nearly all other formal steps; for instance, the IRS requires your business to be legally formed with the state before you can apply for an EIN. This is also a great point in our journey to call out, you likely are more than capable of filing your LLC origination documents yourself with the Secretary of State. A word for the wary: if you google “File an LLC” or something similar you will be flooded with roadside bill boards offering to do this for free (They may do it for free but you still pay the state fee). The cost will be upsells on points we touch on down the road.

The Vehicle Identification Number (Your EIN)

An Employer Identification Number (EIN) is a unique nine-digit number issued by the IRS to identify your business for tax purposes. It is essentially your business’s Social Security Number. An EIN is not technically required for all LLCs, unless you have employees, but it is necessary to open a dedicated business bank account, or dedicated business credit card (an important step, like checking the air in your tires).

Think of the EIN as your vehicle’s unique VIN. No bank will finance a car without a VIN, and no bank will open an account for your business without an EIN. At this point in our journey I want to stress one critical point: obtaining an EIN from the official IRS.gov website is absolutely free and takes less than 15 minutes. Beware of third-party services that charge a fee for this; they are simply filling out the same free form on your behalf and are an unnecessary expense for any new business owner.

The Owner’s Manual (The Operating Agreement)

An Operating Agreement is the internal rulebook for your LLC. It is a private legal document that outlines how your business will be run, who has management authority, how profits will be distributed, and what happens if the business closes.

This is the owner’s manual for your unique vehicle. It details how the engine works, who is authorized to drive it, and what to do if it breaks down. A common mistake is assuming a single-member LLC doesn’t need one. This is false. Banks, lenders, potential investors, and even courts will demand to see this “manual” to understand how your business is governed and to confirm it is being treated as a legitimate entity separate from its owner. Without a well-drafted Operating Agreement, you risk being denied financing and may weaken the very liability protection you sought by forming an LLC in the first place.

My callout at this point in our journey is the use of templates. Those bill boards I mentioned earlier? They will provide you with a template, or you can find a template online. While this is better than nothing, your business, and your assets are unique. A well tailored Operating Agreement is pivotal to your liability protection. Use the wrong Owners Manual to fix your car and you are causing more harm than good.

Part 3: Fuel, Insurance, and Financial Systems: Powering Your Operations

A legally formed vehicle is useless without the systems that make it run. For your business, this means establishing a dedicated fuel source (a bank account), understanding your mandatory insurance (tax obligations), and consistently maintaining the separation between your business and personal finances. The legal documents create the potential for protection, but it is your disciplined actions that make that protection real.

The Fuel Tank (The Business Bank Account)

For any business, Sole proprietor (DBA), or LLC, a separate, dedicated bank account is non-negotiable. Mixing your business and personal funds in one account, a practice known as “commingling,” is one of the fastest and most certain ways to destroy your liability protection as an LLC. If you are a Sole proprietor you still want to have a separate account for tax time without one you face a traffic jam when trying to decipher what was a business expense.

For LLCs: think of your business bank account as the vehicle’s dedicated fuel tank. Commingling funds is like pouring sugar in the gas tank; it might seem convenient in the moment, but it will seize the engine and void your entire warranty. In legal terms, this is called “piercing the corporate veil,” an action a court can take that makes you personally liable for your business’s debts. Beyond this critical protection, a separate account makes you look professional to clients, dramatically simplifies bookkeeping, and is essential for building a financial history to secure future business loans.

Paying Tolls (Understanding Tax Obligations)

One of the biggest shocks for new entrepreneurs is the self-employment tax. Here is a common misconception I run into: forming an LLC is a legal decision, not a tax savings decision. Regardless of your initial entity you will face taxes as a new operator. You see, when you work for an employer, they pay half of your Social Security and Medicare taxes. When you are self-employed, you are responsible for paying both the employee and employer portions, which amounts to a hefty 15.3% of your net business income.

Think of this tax as paying highway tolls. If you are driving around New England you are going to run into tolls. Well, your not going to be able to run your business without paying taxes. The 15.3% is your base toll. Furthermore, unlike a W-2 employee, these taxes are not withheld automatically. You are required to proactively pay this “toll” to the IRS in four quarterly estimated tax payments throughout the year. Failing to do so will result in penalties, the financial equivalent of being ticketed for driving an uninsured vehicle.

My recommendation for the uninitiated. Set 30% of your net profits aside as soon as you earn it. The government is your biggest silent partner. And they will expect you to pay this or face significant consequences. Now the 30% may be conservative. But it’s better to have the funds then not. Further it disciplines you to run a business that is profitable. Your first year is like driving through fog, and in this scenario your tax obligation is the deer in the headlights. Hopefully by setting aside the 30% every month is like driving with your high beams on, you’ll know the deer is there with plenty of time to brake.

The Mandatory Insurance (Business Liability Coverage)

While taxes are a mandatory cost of being on the road, true business insurance is the policy that protects your vehicle from the financial devastation of a crash. It is the unseen foundation that prevents a single accident from totaling your entire investment. For Massachusetts businesses, two types of coverage are non-negotiable. General Liability (GL) Insurance is the bedrock, covering you for third-party property damage or bodily injury for instance, if a customer slips and falls in your shop. Second, if you have even one employee, Massachusetts law requires you to carry Workers’ Compensation Insurance to cover their medical bills and lost wages if they are injured on the job. Beyond these, businesses that provide advice (like consultants) need Professional Liability (E&O) insurance to protect against claims of negligence, and any business storing customer data should strongly consider Cyber Liability Insurance. Regardless of your entity structure, the best first step is to speak with an independent insurance broker who can assess your specific risks and find the right policy for your business vehicle. Combine a properly running LLC and Business Insurance, and you’ll be driving one of the safest vehicles on the road.

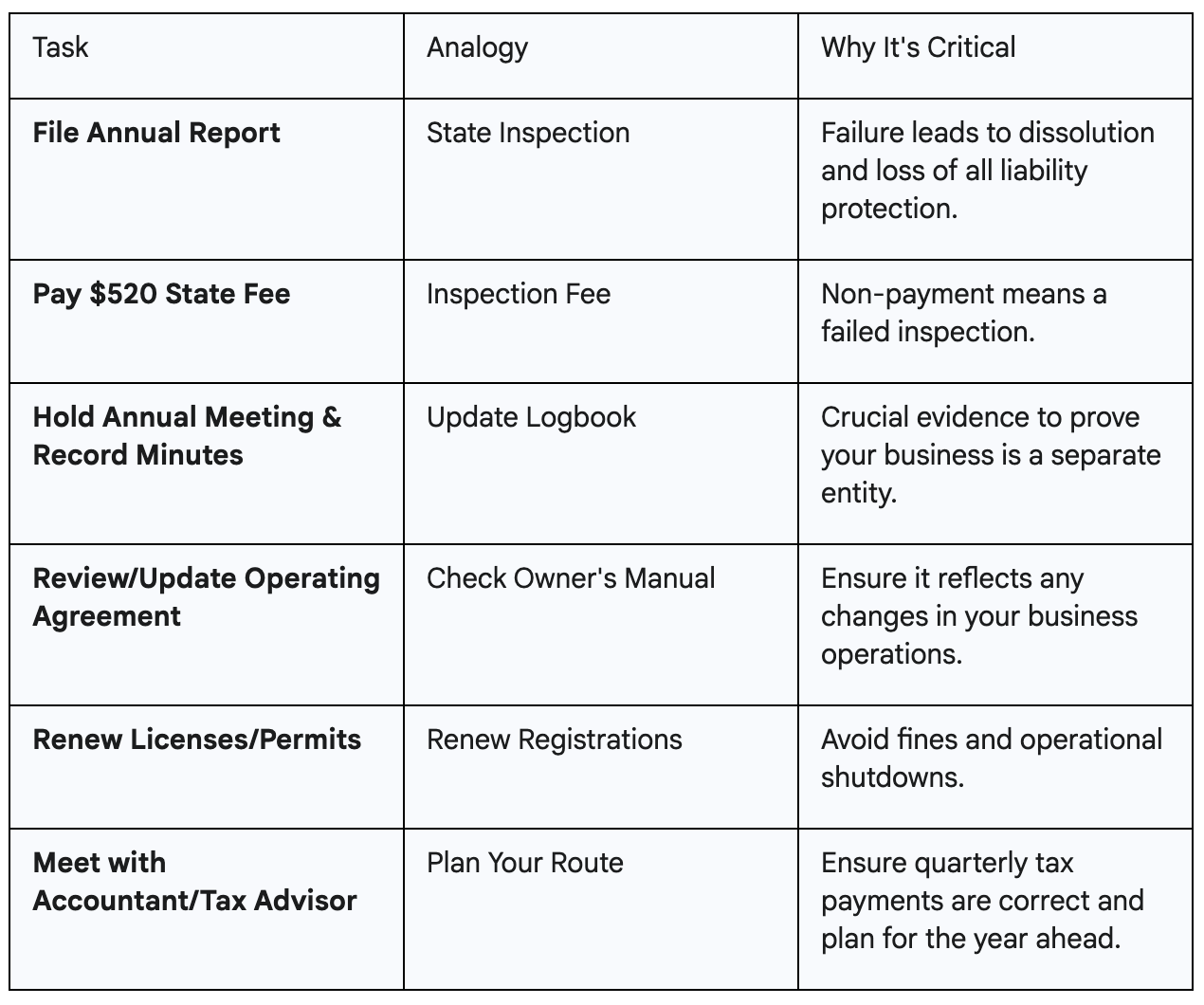

Part 4: The Annual Maintenance Schedule: Ensuring Ongoing Legal Health

Your business vehicle is built, fueled, insured, and on the road. Congratulations, but the job is not over. To ensure a long and successful journey, you must adhere to a strict schedule of regular maintenance. Proactive compliance is what separates thriving businesses from cautionary tales.

The Mandatory State Inspection (The Annual Report)

Every LLC in Massachusetts must file an Annual Report with the Secretary of the Commonwealth on or before the anniversary of its formation date. This is your mandatory annual state inspection. It is not optional, and it comes with that recurring $520 fee. The penalty for failing this inspection is severe: the state can administratively dissolve your LLC, effectively revoking your business registration and erasing your liability protection completely. DBA’s must be refilled according to your town’s schedule. Where I am in Mansfield, for instance, it is every four years.

Checking the Logbook (Annual Meetings & Corporate Formalities)

Even if you are the sole owner of your LLC, holding a brief annual meeting and documenting it with “minutes” is a powerful form of legal protection. This isn’t about bureaucracy; it’s about creating evidence.

This is your vehicle’s maintenance logbook. If you ever get in an accident or decide to sell the car, the first thing an expert will ask for is the service record. These minutes serve as the official log that proves you are a responsible owner who treats the business as a separate legal entity. This documentation is crucial evidence for a court, a lender, or a potential buyer.

Advanced Diagnostics (Hiring, Contracts, and IP)

As your business grows, its maintenance needs become more complex.

- Hiring Mechanics (Employee vs. Contractor): Massachusetts has one of the strictest tests in the country for classifying workers, known as the “ABC Test”. Getting it wrong can lead to crippling penalties and personal liability. The toughest hurdle for most businesses is that a worker can only be an independent contractor if the service they provide is

outside the usual course of your business. For example, a marketing agency cannot hire a “freelance” marketer as a contractor to do marketing work. - Service Agreements (Contracts): Ensure you have clear, written contracts with all clients and vendors. Vague agreements are a primary source of disputes that can stall your business.

- Protecting Your Custom Paint Job (Intellectual Property): Your brand name, logo, and slogans are valuable assets. As you grow, take steps to protect this intellectual property through trademark law to prevent others from using it.

To keep your business in peak condition year after year, follow this simple maintenance schedule.

Part 5: The DIY Route vs. Hiring a Professional: A Final Consideration

With a wealth of online formation services available, the temptation to take the “Do-It-Yourself” route is strong. The primary advantage is clear: cost. Filing the state paperwork yourself or through a low-cost online service is significantly cheaper than hiring an attorney. However, this path has its risks.

Think of it this way: filing the Certificate of Organization is just one part of building your business vehicle. A DIY service will sell you a standard car frame, but it won’t tell you if you really needed a truck. It won’t help you write a custom owner’s manual (your Operating Agreement) or ensure all the safety features are properly installed for the roads you plan to travel. The risks of the DIY approach include choosing the wrong business structure, which can lead to unnecessary tax burdens, and using generic, one-size-fits-all documents that fail to provide real protection when a dispute arises. The most dangerous risk is making a small error in formation or operation that allows a court to “pierce the corporate veil,” destroying your liability protection and putting your personal assets on the line.

Hiring a small business attorney is an upfront investment in getting it right from the start. Or you can consider it as a time saver. i.e. You’re paying for a professional’s time so you can focus on building the business. But more importantly an attorney does more than just file a form; they act as an expert mechanic and guide. They own a professional obligation to their client to ensure the vehicle is road worthy and safe for operation. Not only that, they provide tailored advice on the best business structure for your specific situation, draft a customized Operating Agreement that anticipates future challenges, and ensure you are compliant with all state and federal regulations. While the initial cost is higher, it is often a fraction of the expense required to fix a critical error, defend against a lawsuit, or pay unexpected tax penalties down the road. The choice comes down to your tolerance for risk versus your willingness to invest in a professionally built, legally sound foundation for your business.

Conclusion: Enjoy the Drive, But Don’t Forget the Tune-Ups

The journey from a garage project to a fully operational business vehicle is a major accomplishment. You have successfully navigated the complex assembly of legal structures, federal registrations, and financial systems. But the key to a long and successful road ahead is consistent, proactive maintenance. Legal and financial compliance are not one-time tasks; they are the regular tune-ups that keep your business running smoothly, protect you from unexpected breakdowns, and ensure your journey is a profitable one. As you grow, don’t hesitate to consult with expert mechanics (your attorney and accountant) to keep your business engine in peak condition. I hope this guide gets you started on your journey. In my personal opinion, it’s more costly to never get started, then it is to make a couple mistakes along the way.

This is a contributed blog post written by Nathan T. Harding, a small business and estate planning attorney and the founder of Somnium Advisory in Mansfield, Massachusetts. A former U.S. Navy Officer and IRS Trial Attorney, Nate combines disciplined, real-world experience with deep legal and tax knowledge to help Massachusetts entrepreneurs protect what matters most. He specializes in guiding businesses from formation through ongoing compliance, building strong legal foundations for sustainable growth. Somnium Advisory is a Service-Disabled Veteran-Owned Small Business.

Are you interested in contributing a blog post? Fill out our contact form.

What's the state

of Massachusetts

small businesses in 2026?

Enter your name and email address for our State of Small Business in Massachusetts 2026 report to find out. You'll also receive weekly emails from us!

Leave a Reply